Buyer Representation in Paris – Frequently Asked Questions

Frequently Asked Questions for International Buyers in Paris

Buying property in Paris is very different from purchasing real estate in North America. There is no centralized MLS, buyer representation is not standard, and the process is governed by strict legal steps handled by a notaire.

This FAQ is designed for English-speaking and international buyers—particularly those relocating from the United States, Canada, or abroad—who want clear, reliable answers before entering the Paris property market.

With independent buyer representation, SHOKO provides structure, clarity, and full access to the Paris real estate market, helping you move forward with confidence at every stage of your purchase.

Why Buying Property in Paris Is a Strong Long-Term Investment

Paris remains one of the most stable and desirable real estate markets in the world. Property values have historically shown resilience, particularly in prime arrondissements where demand consistently exceeds supply.

Beyond lifestyle, purchasing property in Paris is a strategic long-term investment. Ownership allows you to build equity while holding a tangible asset in a globally recognized market with strong international demand.

Whether you are purchasing a primary residence, a second home, or an investment property, Paris offers long-term value supported by location, scarcity, and global appeal.

How the Paris Property Market Differs from North America

Unlike the United States or Canada, the Paris real estate market does not operate through a centralized system. Properties are distributed across multiple agencies, private networks, and professional relationships.

Many desirable properties are not fully exposed online or are sold before reaching public platforms. As a result, buyers relying solely on property websites often experience delays, limited access, and incomplete market visibility.

Understanding this structure is essential to navigating the Paris market effectively.

Why Buyer Representation Is Essential in Paris

In France, real estate agents are legally required to represent the seller’s interests. There is no built-in system ensuring that buyers receive dedicated advocacy.

As a buyer’s agent in Paris, SHOKO works exclusively for the buyer. This includes identifying suitable properties, communicating with listing agents, securing access to viewings, and guiding the negotiation process.

This independent representation ensures that your interests are protected, while also giving you access to opportunities that may not be available through traditional channels.

Understanding the True Costs of Buying Property in Paris

Buying property in Paris involves both acquisition costs and ongoing expenses. In addition to the purchase price, buyers should plan for notaire fees, registration taxes, legal costs, and potential financing expenses.

Ongoing costs may include property taxes (taxe foncière), insurance, maintenance, and condominium charges for apartments (co-propriété).

Understanding these costs in advance allows for a structured and financially sound purchase.

Why Mortgage Pre-Approval Matters for Paris Buyers

Obtaining mortgage pre-approval before beginning your property search provides clarity and credibility in the Paris market.

It defines your purchasing capacity and strengthens your position when making an offer. French lenders assess financial stability, income structure, and residency status.

Working with experienced professionals ensures your financing aligns with French requirements and timelines.

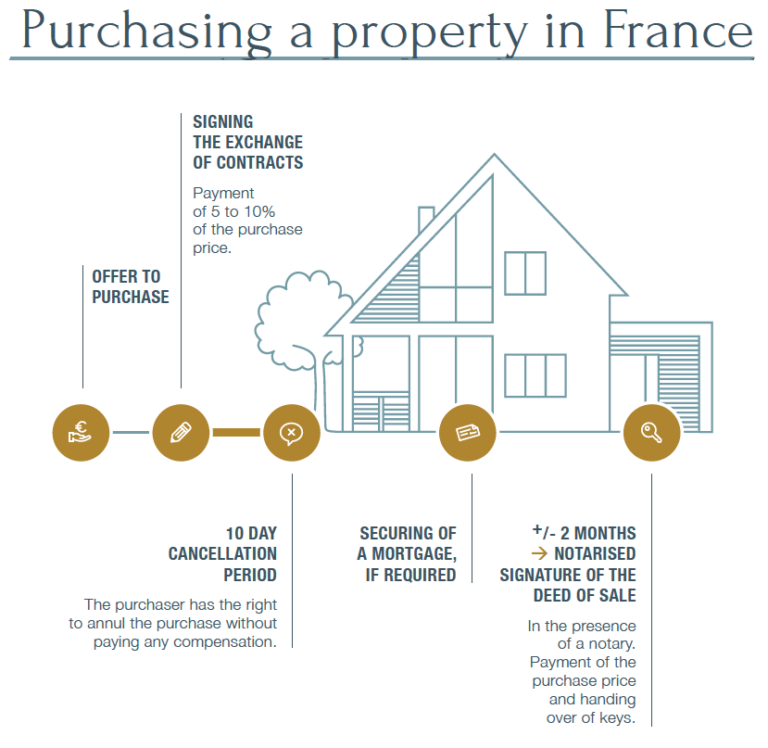

How to Make an Offer on Property in Paris

Making an offer in Paris is a formal and legally binding step. Once accepted, the transaction proceeds toward signing the Compromis de Vente.

Offers may include conditions such as financing approval or specific timelines. Understanding negotiation strategy, legal implications, and market dynamics is essential when submitting an offer.

Professional guidance ensures that your offer is both competitive and aligned with your interests.

The Role of the Notaire in Paris Property Transactions

The notaire plays a central role in every real estate transaction in France. This legal professional ensures compliance, secures funds, and registers ownership with the state.

Funds are held in a regulated escrow account (compte séquestre), providing security and transparency throughout the transaction.

While the notaire represents the legal framework, independent buyer guidance ensures you fully understand every step and document involved.

Buyer-Only Real Estate Guidance in Paris for International Buyers

Combining French market expertise with a North American approach to clarity, strategy, and long-term value

Property Inspections in Paris — What International Buyers Should Know

In France, property inspections differ from North American practices. Sellers are required to provide a series of mandatory diagnostic reports (Dossier de Diagnostic Technique – DDT).

These reports include energy performance (DPE), electrical systems, gas installations, asbestos, lead exposure, and environmental risks.

While these diagnostics provide transparency, many international buyers choose to conduct additional inspections for further reassurance, particularly for older properties or renovation projects.

Home Insurance and Mortgage Protection in France

Home insurance (assurance habitation) is an essential component of property ownership in France. It protects against risks such as fire, water damage, theft, and liability.

For financed purchases, mortgage insurance (assurance emprunteur) is typically required. This insurance protects both the lender and the borrower and can often be customized or sourced independently.

Understanding these protections ensures compliance and long-term financial security.

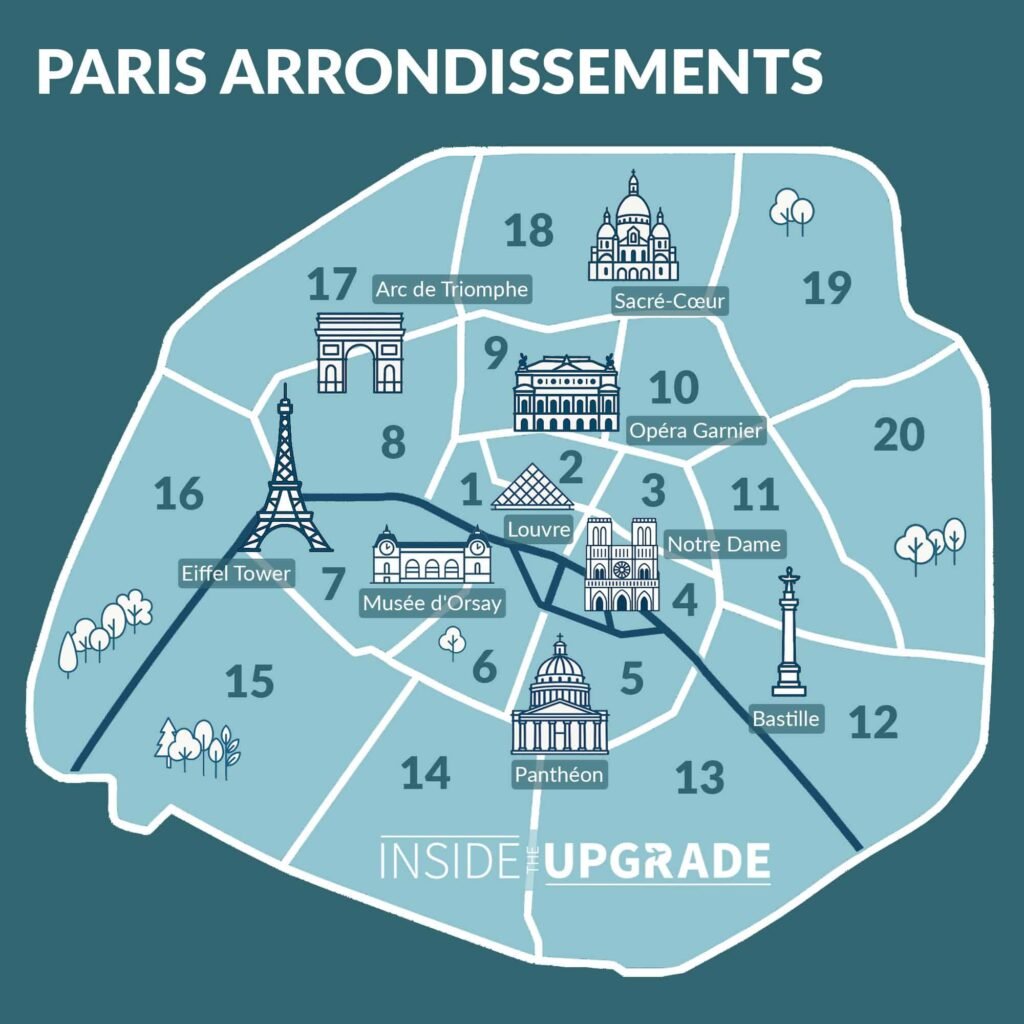

Choosing the Right Neighborhood in Paris

Location is one of the most important factors when buying property in Paris. Each arrondissement offers a different lifestyle, architectural style, and long-term investment profile.

Prime areas such as the 7th, 8th, and 16th arrondissements are particularly sought after for their stability, prestige, and strong resale value.

Choosing the right neighborhood requires balancing lifestyle preferences with long-term market considerations.

Accessibility and Lifestyle Considerations in Paris

Paris offers one of the most efficient public transportation systems in Europe, allowing residents to live comfortably without relying on a car.

Proximity to metro lines, schools, shops, healthcare, and cultural institutions significantly impacts both daily quality of life and property value.

Accessibility remains a key factor in both lifestyle and long-term investment performance.

Buying Property in Paris with Resale Value in Mind

Even when purchasing for personal use, it is important to consider resale value.

Factors such as location, building quality, layout, natural light, and energy performance all influence long-term desirability.

Properties in well-maintained buildings and established neighborhoods tend to retain value more consistently over time.

Making informed decisions at the time of purchase protects your investment for the future.

How SHOKO Supports International Buyers in Paris

Navigating the Paris property market requires coordination, access, and strategy.

SHOKO provides a centralized and structured approach, managing communication with agencies, identifying relevant opportunities, and guiding clients through every step of the process.

This approach eliminates fragmentation, reduces delays, and ensures that international buyers can move forward with clarity and confidence.

When You Are Ready to Begin Your Paris Property Search

If you are considering purchasing property in Paris, the first step is a private consultation.

This allows for a clear understanding of your objectives, budget, and timeline before entering the market.

In Paris, the most desirable properties are often accessed through professional networks rather than public listings.

With the right guidance, you gain both access and a strategic advantage.